Sasol [JSE:SOL], "BEE calm and remain invested"

Energy:

Sasol

“BEE calm and remain invested”

Share price: R372,00

Net shares in issue: 610,7 million

Market cap: R227,2 billion

Forward PE F2018: 13,0x

Forward PE F2019: 12,3x

Forward dividend yield year one: 2,7%

Fair value and target price: maintained in the region of R400

Trading Buy and Portfolio Buy (recommendation of selling rallies into strength remains)

The Inzalo black empowerment transaction wraps up in June 2018 and assuming the current share price range prevails, there is no transfer of ownership and a cash deficit. The proposed new Khanyisa transaction gives 20% direct black ownership in Sasol South Africa Pty Ltd for a period of up to ten years which, together with black ownership at Sasol, results in a total 25% black ownership in Sasol South Africa for the Khanyisa empowerment period. I had applied a guestimate previously to a possible effect on shares in issue and thus earnings per share, which were below consensus estimates, so the announcement makes a negligible difference to my estimates and underlying fair value. The Sasol share price took a pounding after the announcement, down over 6% on Wednesday, but this is an overreaction and investors should remain invested, seeing the lower level as a relatively good new entry point. This note unpacks the salient points on Inzalo and Khanyisa.

What you need to know

Inzalo was implemented in 2008 with beneficiaries acquiring Inzalo shares at R366. There are six component pieces. Unlike Inzalo, the fact that the new transaction is independent of the share price means an element of derisking.

The issue of new shares to wrap up Inzalo would have a one-off dilution in 2019 of 5%. This I have already factored in to my valuation.

At the end of June 2017, Sasol had R12 billion in debt arising from preference shares issued by Inzalo BEE entities. The Sasol shares held as security for this debt had a spot value of around R9,5 billion. Sasol consolidates the debt on its balance sheet. The deficit is R4 per Sasol share.

Khanyisa will have a further dilution of up to 2% from an increased number of shares in the early years. Share based payment charges under IFRS2 also effects future reported earnings.

The full dilution in 2028 is also a function of the value of Sasol South Africa at that time. Khanyisa will use the Sasol BEE share, SOLBE1, for empowerment qualification thereafter. Those involved can sell their SOLBE1 to other BEE shareholders.

Sasol will have to issue about 34 million shares to raise cash to repurchase Inzalo entity shares and fund the deficit in Inzalo. This will only happen after shareholders vote on the new transaction in November. The issue is 5% of the current shares in issue.

As the new shares are included for EPS purposes in the denominator after 2018, shares in issue will be approximately 645 million rather than 611 million.

Also, 2,8 million cash offer Inzalo shares rank equally to Sasol shares and these will convert to ordinary shares.

However, as I have had a rough estimate of 30 million shares and have allowed for that in EPS estimates and valuation, the announcement has only a small effect on my numbers.

Sasol staff acquire a 9,8% shareholding in the Sasol South African assets. This is worth R9 billion and is vendor financed by Sasol South Africa. As these mature assets pay out the bulk of earnings in dividends, the dividends received by the share ownership plan will repay and service debt.

The Khanyisa public scheme open to black members of the public is also 9,8% and worth R9 billion and vendor financed by Sasol, with dividends being applied in the same way.

When the debt in the empowerment entities is paid down in ten years, the shareholding in Sasol South Africa is exchanged for Sasol BEE shares. These shares don’t convert to Sasol ordinary shares.

If I take both the staff and public scheme it equals 19,6% with a total value R18 billion. This implies that the Sasol South Africa businesses are valued at R91 billion on a 100% basis. There is also total debt of R88 billion, of which R46 billion is an interest free shareholder loan from Sasol Limited to Sasol South Africa.

To maintain Sasol BEE shares in circulation shareholders in SOLBE1 are incentivised to waive a right to convert shares to ordinary shares by receiving 35 new BEE shares for each 100 Sasol shares held. The maximum number of new BEE shares is 1 million.

Sasol Inzalo shareholders who don’t get a shareholding out of Inzalo receive one SOLBE1 share for every ten Inzalo shares. They also receive a Khanyisa share for every Inzalo share. The number of new BEE shares is 2,8 million.

Staff in the Inzalo scheme receive shares worth R100 000 each. Black shareholders can elect to receive ordinary shares or SOLBE1 shares and those not classified black receive ordinary shares. These shares receive dividends and vest after three years. The total is 5 million shares.

So, the total of the three tranches above is 8,8 million shares.

Sasol is assuming 15% of the SOLBE1 shareholders will accept and that 100% of the Inzalo shareholders and staff receive shares. This makes for an extra 2,9 million shares in 2019 and the 5 million staff shares in issue from 2021.

Due to the Khanyisa transaction and the issue of shares there is an IFRS2 share based payment charge of R7,3 billion over the term of transaction. It is important to note that this is non-cash although it will affect reported earnings. So, I’d back this charge out to get a sense of underlying operational earnings.

Assuming an IFRS2 charge of R3,7 billion (50%) or R6 per share in 2018 that would be the equivalent of 17% of 2017 headline earnings. It is then 10% per year in 2019 through 2021 with balance split over the transaction term.

The earnings and value effect of Inzalo is a given at about 5% so there should be no reaction in the stock market if this had been properly evaluated.

However, whilst we know the immediate financial effect of Khanyisa, it is a bit hazy beyond 2028. The new number of shares issued in 2028 will be a function of the value attached to South African assets, the Sasol share price, and if there is going to be BEE share discount.

In a static scenario, 2018 EPS is going to be 17% to 20% lower because of the IFRS2 charge, 2019 EPS is about 5% lower because of 2,9 million new shares, and EPS from 2021 is about 2% lower.

But I emphasise static as Sasol earnings are very sensitive anyway to changes in the oil price and rand exchange rate. A $1/bbl move in the annual average crude oil price would affect EPS by about R1 per share or 3% of 2017 EPS anyway, whilst a 10 cent move up or down in the annual average rand/ dollar exchange rate would have a roughly 70 cents per share or 2% effect on earnings. In this context, the BEE effects are quite modest.

Also, the BEE deals positively affect net asset value by 6,6% in rand as is broadly flat in cents per share. Sasol ended June 2017 with shareholder equity of R212 billion or 348 cents per share. Assuming the deals are in place immediately net asset value increases by R14 billion to R226 billion and NAV per share on the 645 million shares is 350 cents.

The debt to equity ratio improves on this deal too, falling to 20% from 27%.

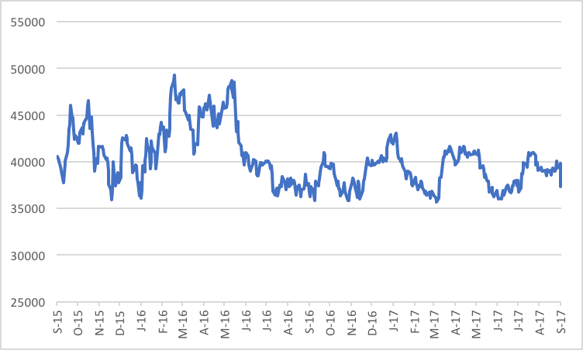

Chart: Sasol share price in ZA cents

Recommendation

I hold to the view of selling rallies in to strength. I observed before that the stock was too cheap at levels closer to R350, on current earnings variables. Fair value and target price maintained in the region of R400 on longer run considerations, notwithstanding Khanyisa.

Wishing you profitable investing, until next time.

Mark N Ingham

Read more fundamentals by Mark Ingham:

- Brait

- Sibanye

- Barclays

- Sun International

- Telkom

- Sasol

- Naspers

- Woolworths

- Attaq

- AngloGold Ashanti

- Massmart

- Bidvest