The JSE started the week on the backfoot as it closed weaker on Monday on the back of losses in the industrials and financials indices.

The local bourse diverted from earlier trends in Asia where the major indices closed mostly higher primarily on the back of better than expected Chinese Caixin manufacturing PMI data. The Nikkei surged 1.01%, while the Shanghai Composite Index and the Hang Seng added 0.19% and 0.37% respectively. Despite mostly better than expected manufacturing data for most members of the European bloc, stocks in that region traded mostly lower. US equity markets opened marginally softer as Donald Trump resumed his calls for the Fed to loosen its monetary policy further.

Locally, there was disappointment in terms of economic data as the ABSA manufacturing PMI recording for November fell to 47.7 from a prior recording of 48.1. The rand retreated briefly from Friday’s highs as it fell to a session low of R14.71/$. At 17.00 CAT, the rand was trading 0.08% softer at R14.65/$.

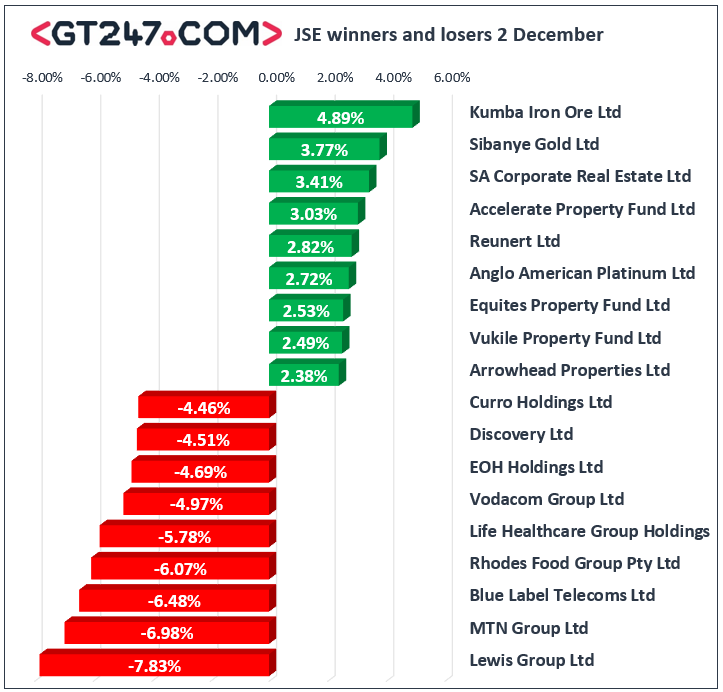

On the JSE, South Africa’s biggest telecom providers came under the spotlight as news broke out that they may face prosecution if they don’t comply with new regulations to cut data prices. MTN Group [JSE:MTN] tumbled 6.98% to close at R85.92, while Vodacom [JSE:VOD] fell 4.97% to close at R115.10. Blue Label Telecoms [JSE:BLU] wasn’t spurred as it dropped 6.48% to close at R3.03, while Telkom [JSE:TKG] closed at R44.93 after losing 4.18%. Retailers recorded another lukewarm trading session as declines were recorded for Lewis Group [JSE:LEW] which weakened by 7.83% to close at R31.30, as well as Woolworths [JSE:WHL] which retreated 3.43% to close at R50.39. Discovery Ltd [JSE:DSY] came under pressure as it lost 4.51% to close at R112.73, while Prosus [JSE:PRX] dropped 2.78% to close at R972.53. Healthcare stocks traded softer as well with declines being recorded for Life Healthcare [JSE:LHC] which closed 5.78% lower at R23.29, and Netcare [JSE:NTC] which closed at R19.13 after falling 4.35%.

Miners recorded some of the day’s biggest advances which saw stocks such as Kumba Iron Ore [JSE:KIO] surge 4.89% to close at R394.26, while Sibanye Gold [JSE:SGL] gained 3.77% to close at R29.97. Listed property stocks tracked mostly higher on the day. SA Corporate Real Estate advanced 3.41% to close at R3.34, Accelerate Property Fund [JSE:APF] added 3.03% to close at R1.70, and Vukile Property Fund [JSE:VKE] rose 2.49% to close at R20.19. Rand hedge, Sappi [JSE:SAP] gained 2.36% to close at R40.79, while Bid Corporation [JSE:BID] added 1.31% to close at R326.85. Gains were also recorded for BHP Group [JSE:BHP] which gained 0.66% to close at R326.70, and Gold Fields [JSE:GFI] which rose 1.045 to R77.75.

The JSE All-Share index eventually closed 0.98% weaker while the JSE Top-40 index lost 0.99%. The Resources index was the only major index to close firmer as it gained 0.51%. The Industrials and Financials indices fell 1.84% and 1.26% respectively.

Brent crude recovered from Friday’s slump in today’s session before it was recorded trading 1.87% firmer at $61.63/barrel just after the JSE close.

At 17.00 CAT, Palladium was up 0.8% at $1855.90/Oz, Platinum had gained 0.28% to trade at $898.70/Oz, and Gold was 0.01% softer at $1463.36/Oz.

Disclaimer:

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by GT247.com at GT247 (Pty) Ltd t/a GT247.com (“GT247.com”) as general market commentary, and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. GT247.com does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information which we receive from third party data providers. You must rely solely upon your own judgment in all aspects of your trading decisions and all trades are made at your own risk. GT247.com and any of its employees will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.